America’s housing market may soon be facing its next bubble as home prices across the country continue to be fueled by demand, speculation and lavish spending that could result in a collapse. Moreover, many homeowners are opting to stay put due to climbing mortgage rates, creating a housing shortage.

Data from the Federal National Mortgage Association, commonly known as Fannie Mae, found that 92% of homeowners think their current home is affordable. Yet, findings further show that 69% of the general population, consisting of both homeowners and renters, believe it’s becoming too difficult to find affordable housing.

Web3 and the real-estate market

While the fate of the United States housing market remains unclear, the rise of Web3 business models based around nonfungible tokens (NFTs), blockchain technology and cryptocurrency aim to solve many of the problems currently plaguing America’s trillion-dollar real estate market.

Jerry Chu, CEO of tokenization platform Lofty AI, told Cointelegraph that although real estate is one of the best asset classes for wealth creation across the globe, most people can’t access it due to three main reasons:

“Real estate, especially today, is expensive. Even if someone could get a mortgage, many times a down payment requires too much cash. The real estate process is also frustrating, as mortgages need to be approved and a title escrow process could take up to 60 days. Finally, there isn’t much liquidity in real estate, therefore sellers will likely lose money if they wish to quickly liquidate.”

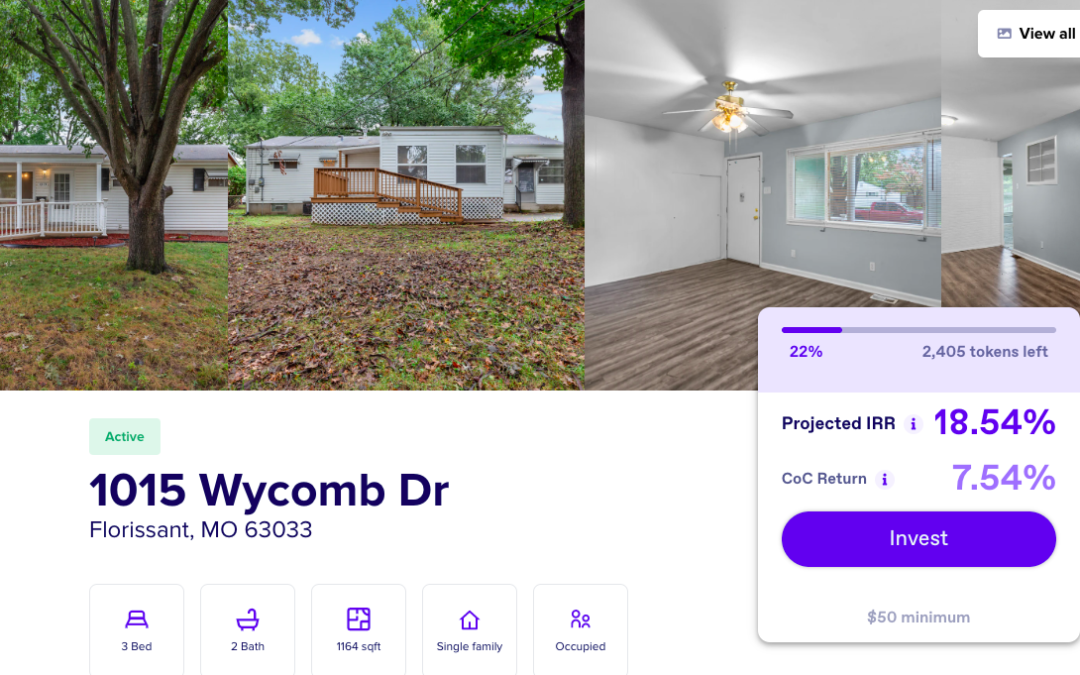

In order to make real estate attainable for the masses, Chu decided to create a platform that could fractionalize properties. Known as Lofty AI, Chu explained that the platform is built on the Algorand blockchain and consists of various turnkey rental properties that multiple investors can fractionally purchase for as little as $50. “You can think of every property as its own mini blockchain on the Algorand network. Assets, or unique tokens, are created for every property listed. The token supply is different depending on how expensive the properties are,” said Chu.

While the concept of tokenizing real estate has become rather common — for instance, Cointelegraph research recently found that thereal estate sector makes up 89% of all traded security tokens — Chu pointed out that Lofty is an active investing platform. “Similar platforms invest in real estate and flip properties to customers, but we allow investors to manage these properties and continually earn rewards and income.”

Elaborating on this, Chu explained that Lofty is based on a co-ownership model where the deeds for each property listed on the marketplace are held and owned by a limited liability company, or LLC. When investors purchase tokens, they immediately become a member of that entity, meaning they own a percentage of that business.

Like other decentralized finance (DeFi) platforms, Lofty has a governance system that allows token holders to vote on how to manage the properties they own. “Token holders need to reach a supermajority vote of 60% for decisions to be acted upon. The winning vote is then sent to the property manager to carry out. These decisions could include maintenance, rent changes, eviction decisions and more.”

Chu added that investors can also earn portions of rental income generated from tenants, which can either be withdrawn to a bank account or donated to Mercy Housing, an affordable housing organization. “Most Lofty users care about the appreciation of their tokens on the properties they buy into, and, therefore, donate their earned income to affordable housing programs,” Chu mentioned.

While this may be, Chu emphasized that the goal behind Lofty is to make real estate investing more accessible simply. “This seems to be the case, as the platform launched last year and already has close to 4,000 users,” he said. Takahito Torimoto, a solutions architect and Lofty user, further told Cointelegraph that he has been a real estate investor for a few years, but Lofty has been an ideal solution due to the platform’s liquidity and returns. “There are no fees for users, and given the current real estate market, Lofty appears much better for a very big part of my ‘early retirement’ strategy,” he remarked.

In addition to Lofty, mortgage lender LoanSnap launched a mortgage-backed stablecoin on their Bacon Protocol at the end of last year. Karl Jacob, CEO of LoanSnap and co-founder of Bacon Protocol, told Cointelegraph that while a mortgage-backed token solves many issues associated with stablecoins, these digital assets also benefit current homeowners and buyers.

Technically speaking, LoanSnap has minted NFTs tied to individual mortgage liens, which are property ownership rights that collateralize mortgage loans. Those NFTs are then used to back LoanSnap’s stablecoin known as the “bHome token.” Jacob explained that this system is beneficial for a number of reasons:

“Mortgage-backed stablecoins are advantageous to homeowners and buyers because speed is everything in a real-estate transaction. This process works quickly since it leverages the Ethereum blockchain. You can see a loan getting closed and funded in a matter of 24-hours or less, depending on state compliance.”

In other words, wrapping an NFT around a mortgage lien and putting that asset on a blockchain network allows anyone access to those records. “We provide the minimal amount of data, so individuals can only see the address of a property, the lien size and property value,” said Jacob.

Jacob claimed that the bHome stablecoin also opens up access to the U.S. housing market. “Investors that buy into the bHome token are gaining exposure to the housing market without having to own a home. This is simply a pool of mortgages across the country that offers a great way to participate without the costs associated with homeownership.” While the platform is fairly new, Jacob shared that about 30 mortgages on LoanSnap are being used for its stablecoin pool, noting that the platform has lent out over $7 million against its $42 million home value on the platform.

Some U.S. real estate properties have also recently been sold as NFTs, a concept that seems to be attracting Generation-Z homebuyers. This is important, as data shows that Gen Z’s only made up 2% of all home sales in 2020. Natalia Karayaneva, CEO and co-founder of Propy — a blockchain-based real estate platform — told Cointelegraph that Propy hasrecently sold three NFT properties: one in Kyiv and two in Florida. “We are the first platform to sell real estate as NFTs, which has resulted in a number of benefits for first-time buyers and sellers,” said Karayaneva.

On a technical level, Karayaneva explained that Propy is able to do this by selling tokenized LLC properties. The purchase records for each property live on the Ethereum blockchain. Once a property sells, the ownership rights are transferred as an NFT to the homebuyer’s wallet address. Karayaneva elaborated:

“The most recent NFT property that sold in Tampa was purchased using the USD Coin stablecoin. Bidding happened in real-time and ownership was transferred in 15 minutes upon closing the sale, which simplifies and speeds up the entire traditional home buying process. This is important because the U.S. housing market is so competitive today that people don’t have time to wait. NFT properties are also fully transparent, so prospective buyers can make informed decisions by seeing any appraisals, contingencies and anything else up front.”

Given the transparency and fast-paced nature of NFT home sales, Karayaneva mentioned that the concept is particularly appealing to the younger generation. “The two properties we sold in Florida attracted many Gen Z’s since you can now buy a house with the click of a button,” she said. Karayaneva added that older clients have expressed interest regarding how secure this process is since everything is recorded on an immutable blockchain ledger.

Giving homeowners access to their data with NFTs

Blockchain Home Registry (BHR) is yet another Web3 project using NFTs to represent homeownership. BHR is a DeFi platform built on the Ethereum blockchain that allows homeowners to claim a verified NFT of their property, giving them access to a permanent, transferrable historical record of their home. James Rogers, CEO of Torii Homes — a real estate technology company that developed BHR — told Cointelegraph:

“While people today own their homes, they don’t own the data associated with it. For example, a title company often knows more about an owner’s home history than they do.There is an opportunity for the entire real estate industry to collaborate with homeowners to make sure individuals own the data associated with their homes.”

Rogers explained that BHR allows homeowners to claim their home as a verified NFT upon completion of a thorough Know Your Customer (KYC) process. Once verified, homeowners’ NFTs are placed on the BHR platform, which then allows for organizations across the real estate industry to build services by consuming data from the platform. This allows both organizations and homeowners the ability to monetize their data.

Zach Gorman, co-founder of Torri Homes, told Cointelegraph that homeowners are able to see all their home documents in a dashboard on the BHR platform. “Homeowners can add and maintain their records over time and can then choose to monetize that data by letting other organizations access it.” For example, Gorman explained that an insurance company could more efficiently quote policies using data about homes listed on BHR:

“At the same time, the data added would inform homeowners about risks such as fire or flood that they could face. And, when another insurance company builds an integration on top of the data added, they would compensate the first company for their data. Even if the homeowner chooses to work with the latter company, the former still wins, as well.”

Gorman added that although BHR just launched on April 26, a number of homeowners and service providers have expressed interest in using the platform. “The power of data has never been put on the table before for homeowners, so this is a huge opportunity to democratize that and put power back into homeowners’ hands.”

Challenges may hamper adoption

While Web3 solutions may help solve many of the challenges currently facing homeowners and buyers, it remains questionable as to how the mainstream will react to these innovations.

For instance, Karayaneva shared that properties sold as NFTs through Propy must be purchased using the USD Coin (USDC) stablecoin, yet this may be challenging for non-crypto natives. Even though Karayaneva mentioned that Propy helps facilitate the transfer of fiat to USDC, users who wish to buy an NFT home may also find it difficult due to the fact that loans cannot be taken out. “Currently, we are only accepting full cash offers, but we are working on incorporating a solution to get crypto enabled mortgages on the spot,” said Karayaneva.

Moreover, getting the mainstream to adopt blockchain solutions may also be complicated. For instance, Rogers explained that BHR is initially launching with MetaMask. Although it’s notable that MetaMask’s monthly average user base is growing, MetaMask and other popularcrypto wallets are vulnerable to malware attacks and hacks.

From a technical perspective, it’s important to point out that most of the Web3 solutions mentioned are based on the Ethereum blockchain, which is infamous for high gas fees. Jacob shared that, while using the Ethereum network has been beneficial for Bacon Protocol, the team behind the project has worked hard to hide high gas fees from bHome purchasers. On the other hand, Chu said that he chose to build Lofty on the Algorand blockchain due to its low gas fees. “Lofty sends small transfers to user’s wallets regularly, so if this was built on another chain with high gas fees that would cost much more,” he said.

Finally, it’s important to point out that legal issues may arise when applying NFTs and DeFi standards to real estate transactions. With this in mind, Jacob shared that LoanSnap conducted massive amounts of research when considering the regulatory components associated with a mortgage-backed stablecoin. “LoanSnap is regulated and audited by the state, so we already have regulations in place. The question people ask is if this is a security, but the interesting thing about mortgages is that they are not securities.”

Challenges aside, Rogers said that homeowners and buyers using Web3 solutions like BHR don’t need to fully understand the components behind the platforms, they just need to know that they work. “When I explain BHR, people are interested even if they don’t know much about NFTs and blockchain. The idea here is to onboard new users to the Web3 space and transform the traditional real estate industry. That is what excites us.”

steals Dogecoin’s thunder")