The crypto market has been on a downward trajectory since the tail end of 2021. In early May 2022, it culminated in a dip that impacted traditional markets just as hard. The recent bust removed some speculation from the market. But the shakeup is different than in the past. There are still many more active users utilizing the Bitcoin network than we have seen in past cycles. Many more holders and true believers made it through to the other side. However, as this increases over time, one of the concerns some have over Bitcoin (BTC) may impact its adoption. There is an economic incentive, not just utility, that privacy coins can offer as a solution.

At different points in the first half of 2022, both in crypto market rallies and huge dumps, privacy coins such as Monero (XMR), Dash (DASH) and Zcash (ZEC) have fared relatively well against other altcoins. Does this mean there is an underlying demand for interest in crypto privacy?

The Bitcoin standard is finally here (well, not yet)

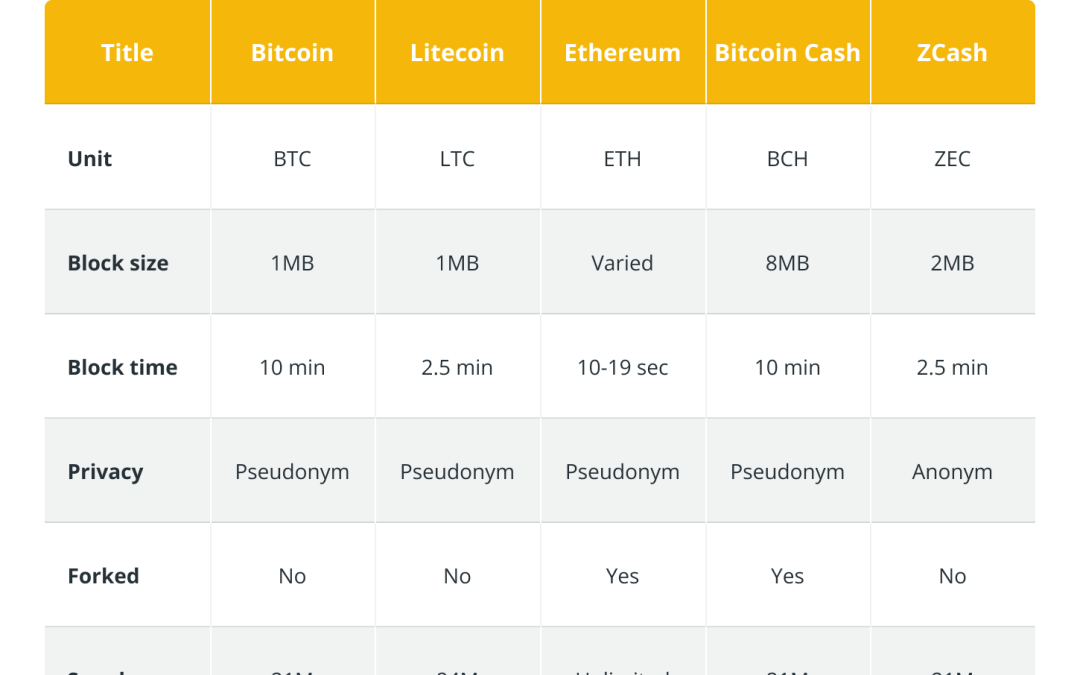

For the sake of this discussion, let us presume that Bitcoin made it. Bitcoin is now the dominant currency globally. But due to the pseudo-anonymous nature of the Bitcoin blockchain, anyone can see all of the transactions for each wallet. And for each coffee purchased, the spending habits of the buyer, the location where the spending took place and all the other dystopian trappings of a 1984-inspired nightmare are a reality. This nightmare is what has spurred on the creation of the likes of Monero, Zcash, Dash, Decred (DCR), Secret (SCRT) and Horizen (ZEN), just to name a few. Some of these have similar qualities to Bitcoin. Zcash is modeled very similarly to Bitcoin with a 21 million hard cap supply and operates by proof-of-work.

Could it be out of the question that one or two of these blockchain protocols would be adopted as the “everyday” transactional currency to complement the Bitcoin standard? Protocols like Monero and Zcash have either a shallow inflation rate or a capped supply. They act with their tokenomics and do not promise to do more than be a medium of exchange and store of value, other than, of course, protecting the privacy of the user.

Related: The loss of privacy: Why we must fight for a decentralized future

Bimetallism: What is that, and why does it matter?

Bimetallism is a concept from long ago and before the advent of cryptocurrencies. As the name suggests, the idea behind bimetallism is that different types of precious metals would be used to offset the price inflation rate relative to the other. Gold traditionally had silver and vice versa to balance the other out if one started to have too much buying power. For example, a horse is worth one gold coin or 10 silver ones (gold and silver are rare to different degrees but still have different intrinsic qualities for utility). If the horse is now equal to two gold a year later, it may only be 12 silver coins, which makes the trade more palatable to the holder of silver, putting pressure on the inflation price of gold. This bimetallism arrangement works in theory when you have similar mediums of exchange like two precious metals. When the state introduced fiat currency in the mix, Grisham’s Law kicked into effect, and with a vengeance.

Grisham’s Law states that bad money drives out good. If a holder has fiat or Bitcoin, there is a high probability that they will value the good/service less than they do BTC and trade away the fiat, which has a potentially unlimited supply. This means that Bitcoin will sit, unused, in people’s wallets forever, destroying some of the value proposition of sound decentralized money for the world. If we are to assume that the world is going to digital mediums of exchange, it will not change the laws of economics.

There will still be adjustments in the price level of things to tradable assets. To keep these different mediums in check, other assets may be needed as alternatives. However, if we do not wish to have Grisham’s Law play out again, there must be assets similar to Bitcoin yet propose a different value proposition. Enter privacy coins.

Related: Gold, Bitcoin or DeFi: How can investors hedge against inflation?

Privacy matters

Bitcoin can be a unit of account, medium of exchange, store of value and other qualities that fit the gold 2.0 narrative. And the traceability of Bitcoin is a good feature that has its uses. As we see now with Bitcoin-backed loans, the transparency of assuring creditors the funds exist is a great utility of the chain. But do you want the coffee barista to know you shop at the antique store every Wednesday? Do you want your personal finance known to your boss? Or to anyone who cares to look through your payment history?

This is where the idea of bimetallism, or “bicryptoism,” can step in and solve these issues. If Bitcoin is adopted with one or two different scarce and limited mediums of exchange (a privacy coin), these can help to keep the purchasing power of goods/services in constant “stable fluctuation” against each other. This is, of course, in the future when Bitcoin is the dominant currency of the world.

Because these different protocols have different properties (just like gold and silver), they can serve different functions in users’ lives. For daily transactions, users can enjoy the privacy that a privacy coin can offer while utilizing all the benefits of a decentralized ledger and blockchain technologies. When users desire to transfer their money into wallets that have a publically facing address, they can choose to keep their funds in Bitcoin. Perhaps, through functions like atomic swaps on-chain, this can be even easier than a decentralized or centralized exchange.

Satoshi Nakamoto, the mysterious inventor(s) of Bitcoin, once wrote: “For greater privacy, it’s best to use Bitcoin addresses only once.” A new BTC address for every user would be rather impractical for the 2022 crypto user, never mind a world where Bitcoin is the standard medium of exchange. Users will either have to try and create a Bitcoin improvement proposal (BIP) to change Bitcoin to adopt to include privacy-enhancing features or co-exist with options in a “bicryptoism” setup with one or more privacy coins. The latter has additional economic benefits of keeping inflationary pressures lower on prices over time.

These are just some thoughts for the future, and the greater crypto community needs to think about these potential issues as we move forward. Economics played a big part in the founding of Bitcoin and the cryptocurrency revolution, and it should be a great source of informing its future as well.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

steals Dogecoin’s thunder")