The bitcoin market appears plagued by negativity after the cryptocurrency lost half its value in 2 1/2 months.

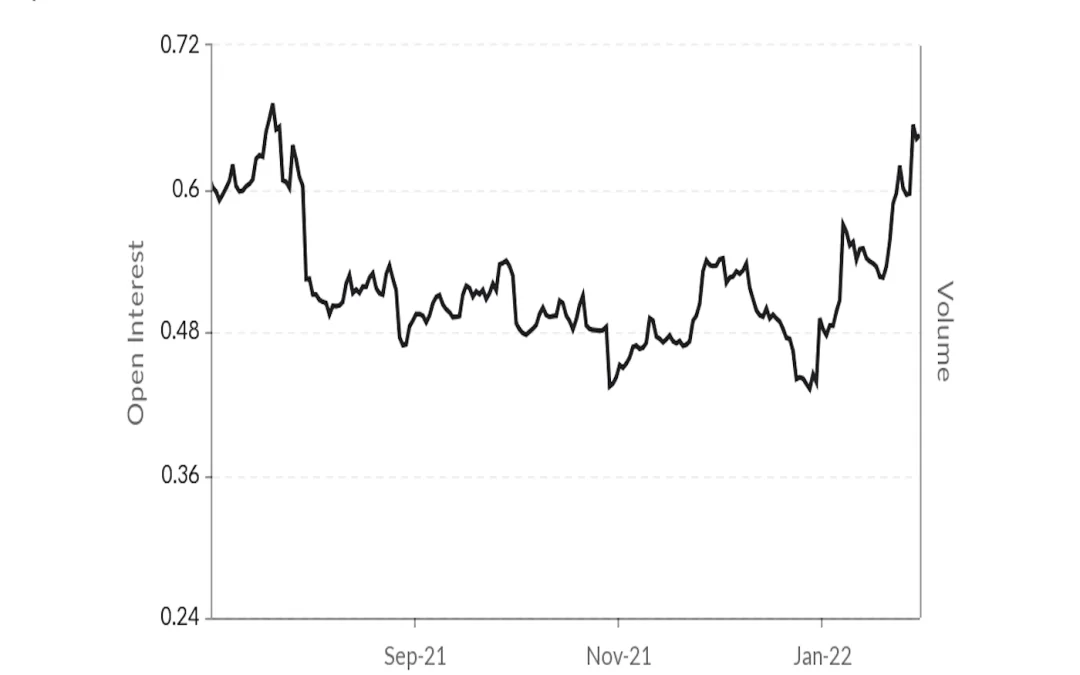

The cryptocurrency’s put-call open interest ratio, which measures the number of open positions in put options relative to those in calls, rose to a six-month high of 0.62 on Sunday, according to data provided by Skew. The ratio was 0.42 earlier this month.

“The put-call ratio suggests demand for puts is currently high,” said Patrick Chu, director of institutional sales and trading at over-the-counter tech platform Paradigm. “We have seen a lot of risk reversal flow recently, where clients were buying puts/ selling calls.”

Traders execute a bearish risk reversal strategy by purchasing puts with lower strike prices and selling higher-strike calls when anticipating a price drop.

A put option gives the purchaser the right, but not the obligation, to sell the underlying asset at a predetermined price on or before a specific date. A put buyer is implicitly bearish on the market, while a call buyer is bullish.

Given the depth of bitcoin’s drop from its Nov. 10 record near $69,000 – it was trading recently about 2.6% down on the day at $36,900 – increased buying of puts is hardly surprising. It might, however, indicate an excess of fear.

Traditional market participants usually use the ratio as a contrary indicator, meaning a sudden surge in the metric is taken to represent the extreme bearish sentiment that’s often seen at the end of bear runs.

Other metrics like the call-put skew, which measures the price differential between calls and puts, are also exhibiting a put bias. The one-week, one-, three- and six-month skews all returned negative values at press time, a sign puts were drawing higher prices than calls, according to data provided by Genesis Volatility.

“The skew is the direction of the options premium,” said Griffin Ardern, a volatility trader from crypto-asset management company Blofin. “When the bearish sentiment is strong, the put option premium is more, and the options skew is negative. When the bullish sentiment is strong, the options skew is positive because the call option premium is more.”

While both the put-call open interest ratio and the skew indicate the same thing, the latter is more reliable, according to Ardern, given it calculates real-time data and is not affected by open contracts. Historically, the six-month call-put skew has been more reliable as a contrary indicator, showing put bias near price bottoms, as observed after the March 2020 crash and the May 2021 slide.

steals Dogecoin’s thunder")