It’s said that 90% of all startups fail, and that we should expect nothing more from ICOs. 10% success rate is still overly optimistic for ICOs, but perhaps not for the reason you may think. You’re probably aware of examples of ICO “founders” who turned out to be a bunch of made up Linkedin-profiles. You’re probably also aware of the risks that comes with sending money to people on the Internet you never met, in an asset or token impossible to freeze.

Also read: Disappearing Premiums Signal Bearish Mid-Term Outlook

Drop The Tokens That Suffer From Overtokenization

You’re probably also aware of the industry-specific risks, apart from straight up scams, which include:

- ICOs violating securities laws

- ICOs using complicated legal structures in order to avoid violating securities laws and having it back-fire

- ICO fundraisers using Ethereum smart contracts and imploding (this actually happened to the Ethereum co-founder himself)

In this post, I’m going to discuss a much more daunting problem that very few seem to grasp; overtokenization.

Let’s be clear: ICOs as a concept is not at all a bad way to fund the development of a new cryptocurrency. However, the ICO space today is overwhelmed by projects that are not even cryptocurrencies. ICOs have moved from covering cryptocurrencies, to apps that uses an existing cryptocurrency as its platform, to regular companies doing something cryptocurrency related, to regular companies doing nothing related to cryptocurrency at all. What many ICO investors seem to forget to ask is: why exactly do these projects need to have a “token”? Somewhere along the way, everything suddenly having a token became normal, and no one barely questions it anymore. This is going to cause a huge problem in the future, and I’m going to explain why.

There are very few cryptocurrency projects that legitimately necessitates a coin or a token from a technological perspective. The known examples that do are the following: actual cryptocurrencies (e.g. Bitcoin, Litecoin, Ethereum, Bitcoin Cash, Monero), and certain protocols involving some kind of game-theoretical token usage (i.e. staking).

One of the few projects from the latter category I can come to think of is Augur. Augur isn’t a cryptocurrency, but a product that uses a cryptocurrency as platform. It’s a decentralized prediction market (currently in beta-stage) consists of a set of smart contracts on the Ethereum blockchain. In Augur, its REP token (an ERC20) is integral to the process of resolving bets. It provides Augur with a way to financially reward and punish the actions of honest and dishonest actors, and creates incentives for a specific category of users (REP holders) to be proactive on the platform.

Augur perhaps isn’t a project without flaws, but what we know is that it isn’t practical to try to create Augur without a token. The token is–from the ground up–integral to the functions of the platform. The token itself is also defensible as an investment: as the popularity of the platform increases, the more revenue will there be for REP holders to earn on fees from resolving bets. I would argue that these ingredients are pretty unique to Augur (and perhaps also similar projects like Gnosis). In fact, there are an extremely limited number of cases of non-cryptocurrencies where a token is both technologically necessary and useful as an investment.

But the allure of launching a project like Augur is tantalizing; you don’t have to plan to create a whole cryptocurrency to launch an ICO, you just need a product that somehow utilizes a token that in some manner economically motivates people to hold it. If you figure out that, then you can launch an ICO too.

Because of the insane amounts of money investors poured into ICOs, every entrepreneur in the industry has quickly decided that whatever project they’re working on should probably involve some kind of token. Because not all projects are launching a new cryptocurrency, and doesn’t involve game-theory or staking that necessitates a token like Augur does, most projects have settled with a model where a specific token is required to utilize its services.

Augur Project

Augur perhaps isn’t a project without flaws, but what we know is that it isn’t practical to try to create Augur without a token. The token is–from the ground up–integral to the functions of the platform. The token itself is also defensible as an investment: as the popularity of the platform increases, the more revenue will there be for REP holders to earn on fees from resolving bets. I would argue that these ingredients are pretty unique to Augur (and perhaps also similar projects like Gnosis). In fact, there are an extremely limited number of cases of non-cryptocurrencies where a token is both technologically necessary and useful as an investment.

But the allure of launching a project like Augur is tantalizing; you don’t have to plan to create a whole cryptocurrency to launch an ICO, you just need a product that somehow utilizes a token that in some manner economically motivates people to hold it. If you figure out that, then you can launch an ICO too.

Because of the insane amounts of money investors poured into ICOs, every entrepreneur in the industry has quickly decided that whatever project they’re working on should probably involve some kind of token. Because not all projects are launching a new cryptocurrency, and they do not involve game-theory or staking that necessitates a token like Augur, most projects have settled with a model where a specific token is required to utilize its services.

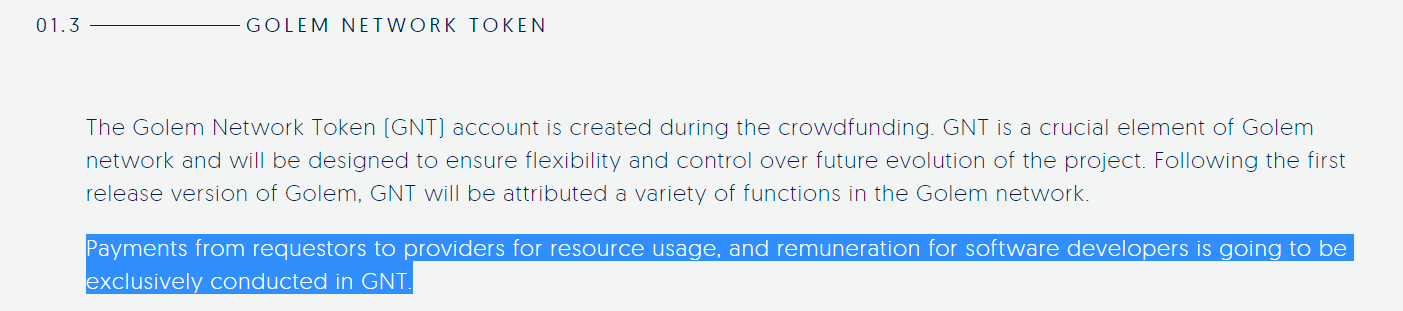

Golem plans to build a decentralized market for computing power.

A Token-Critical Perspective

This is where the industry is running into a problem. Instead of an ecosystem of services being built around cryptocurrencies, you will now have to first purchase a specific token in order to utilize those services. Whether its storage space for rent, processing power for rent or something else, you won’t be able to pay for those things directly in your favorite cryptocurrency, you’ll have to use the specific token they’ve restricted their service to accepting, in order to raise money from you in their token sale.

This restriction severely diminishes the utility of the service they are creating. In the Golem example, its participants will be forced to accept payment in GNT rather than bitcoin for instance. It’s very unlikely that GNT is going to be as liquid as bitcoin, and therefore it is much more likely that the value of GNT will fluctuate spectacularly in comparison, which isn’t very convenient for its users. Furthermore, some sort of micro-economy will have to evolve around the GNT token, that relies on the GNT tokens that are purchased are later resold to the market. That opens up a whole new attack surface, where the entire platform could essentially be hijacked in a coordinated act of market manipulation. This is why absurd constructs such as Bancor have apparead, in order to address this ridiculous problem.

This doesn’t necessarily mean that Golem and the likes of it will be useless; however, there’s a very real chance that something else eventually comes along, providing the same service, but in the currency of its users choosing. Such a competing platform, without the friction of being restricted to a specific token, has a very big edge on its ICO-launched competitor.

My trading tip this week is to go through your portfolio and evaluate your investments from a token-critical perspective. Get rid of those tokens that add no benefit to the product or service they are providing, and in many cases are a down-right handicap. In the end, while it may be true that an ICO could be the thing that gets a project off the ground that wouldn’t have otherwise, it may also be the thing that kills it.

What are your thoughts on market manipulation? Let us know in the comment section below!

Images via Shutterstock, Twitter.

Disclaimer: Bitcoin price articles and markets updates are intended for informational purposes only and should not to be considered as trading advice. Neither Bitcoin.com nor the author is responsible for any losses or gains, as the ultimate decision to conduct a trade is made by the reader. Always remember that only those in possession of the private keys are in control of the “money.”

The post Trading Tip `The Wall´ – Drop Tokens That Suffer From Overtokenization appeared first on Bitcoin News.