In a previous article, I discussed the evolution of Web3 economies and current volatility, focusing on the participatory nature of Web3, which is the foundational technology enabling the creator economy.

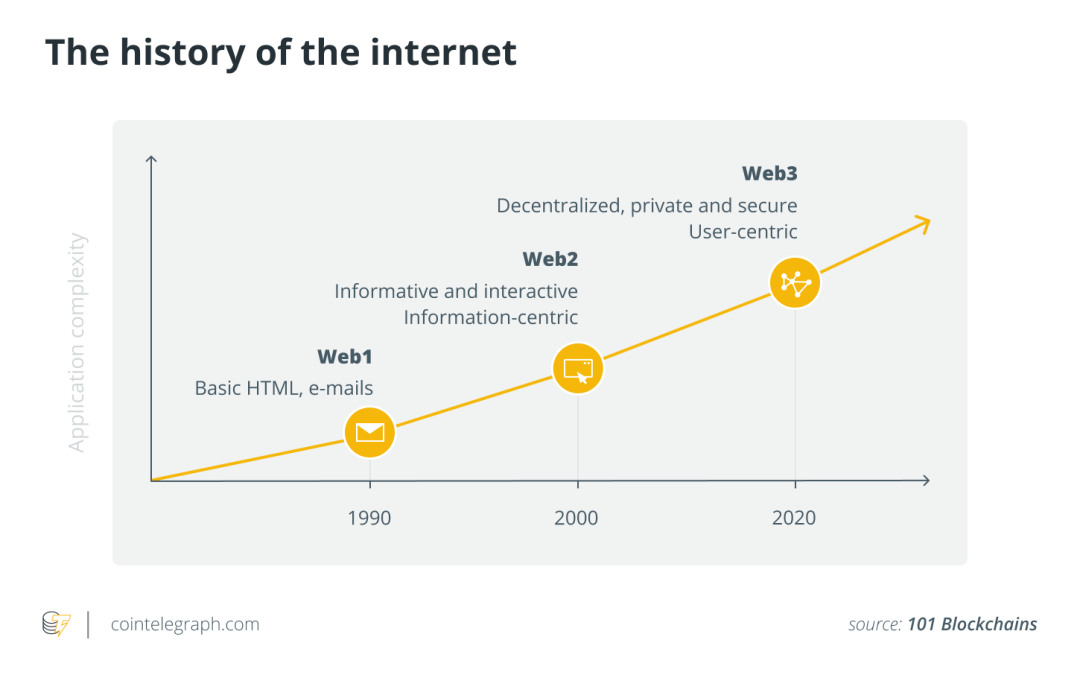

The term “metaverse” — meta and universe — often describes the anticipated future iteration or evolution of the internet powered by Web3 technologies like blockchain and decentralized resource distribution and consumption principles. Although the focus has often been on metaverse modalities such as augmented reality (AR), virtual reality (VR), gaming, Second Life, avatars and so forth, in my view, these modalities represent an interesting evolution or shift from the digital transformation of recent decades to the “transformation of digital.” That is exactly what the Metaverse aims to achieve. It might seem abstract and clunky today, but if we dissect the components that make up the Metaverse, we get a glimpse of a transformed digital future.

Our identity can persist with our avatars and AR/VR representations and be certain, deterministic and applied with non-repudiation. The things we value are represented in the form of tokenized assets with valuation vehicles that not only prevent double-spending but also leverage blockchain as a transaction system, which brings the fundamental tenets of blockchain (trade, trust and ownership) to the Metaverse. The avatars that represent us can interact with various universes and their value systems, and we reserve the right and ability to monetize our data, effort, talent and all the value they generate. And, as our representation traverses various modalities — such as our avatars via VR to in-game representations — we can use things we value and apply that to an economic and value system of our choosing.

Related: Basic and weird: What the Metaverse is like right now

The vision and foundation of metaverse success relies upon seamless interoperability and the transfer of value (tokenized or other semantic web constructs) across universes supported by layer-1 and layer-2 networks. All of this supports the interactive modality I see in the Metaverse. So, we have a lot of work to do. We should look at the commercial aspects of the Metaverse and how it is monetized today and presents an opportunity to conduct business tomorrow.

Monetizing the Metaverse: How do we do business in the Metaverse?

Because Web3 and the Metaverse deal with a construct of tokenized value, we need to look into the financial aspects as a starting point. For instance, an area of my focus is what financial services mean in the Metaverse. We see pervasive financialization of NFTs and the emergence of other asset classes, but what does it mean to monetize the Metaverse? Let us break it down into consumable monetization categories to understand this better.

Category 1: Commercializing protocols

This category represents the current landscape of infrastructure and projects that rely on community development and broader infrastructure development and support services. These projects monetize in the following ways:

- Token-based models: Operation fees to write to the blockchain-powered business network’s distributed database.

- Tokens as a medium of exchange: Lending or selling a token as a “step-through” currency, such as with in-network tokens.

- Asset-pair trading: Monetizing margins.

- Commercialization of the protocol: Technology services including cloud and software labs and consulting services.

- The power of networks: Extrapolating the power of networks and exponential power of co-creation models, leading to new business models and resulting in economic value.

Related: The metaverse will change the paradigm of content creation

Category 2: Simple token sales

While broad, the second category applies to the majority of projects that rely on token sales. Tokens are used as a funding mechanism to fuel development. In many cases, these fit a classical definition of security, which is a token sale with a profit expectation. While these tokens can be viewed as in-network token currency, the expectation is that if they become ubiquitous, that ubiquity subsequently extends itself to fungibility and these tokens take on the status of a currency. These concepts are laden with new terms, definitions and twisted economic models and often face regulatory headwinds, but we are just discussing the state of the industry as it evolves.

One of the subcategories here is nonfungible tokens (NFTs), where the NFT as an asset class begins to surface as a symbol and community belief instrument, valued by a section or subsection of the community. In gaming, for instance, there are game artifacts; in other ecosystems, they represent art, identity or a substrate of a niche social movement. NFTs seem attractive investment instruments with symbolism and cultural obscurity. We have seen this transformation fuel the end goal of the Metaverse, and NFTs have become a de facto representational instrument in the parallel digital realm.

The financialization of NFTs in the digital realm can be compared to an analog to the mobile payments movement triggered by M-Pesa — a concept that started almost two decades ago and in its infancy reached a transaction volume of over $22 million a week with absolutely no financial intermediary, just preloaded conversational minutes traded to move money. While financial institutions salivated at the volume, M-Pesa eventually ended up becoming regulated, and financial institutions got into it via a telco-bank relationship structure. This modality morphed and took the form of actual payments over mobile devices using telco as rails.

Comparing this to the digital realm context, the modality of the Metaverse today is represented by elements of virtual and augmented reality, digital art, gaming and Second Life. The underlying economics involving transfers of value is the real goal and the element that has the power to change the world.

Related: Understanding the systemic shift from digitization to tokenization of financial services

But, as with the M-Pesa case, I want to question and discuss how the current forms of the modality shape the actual form of value transfer and payments.

Category 3: The emerging crypto market structure

The third category is an important one, as it represents the market structure that has the power to facilitate exchange, interoperability and seamless value transfer — all the tokens and forms of valued assets exposed to some form of financial primitives. These basic financial primitives include buying/selling, borrowing/lending/collateralization and others.

Just as in the case of M-Pesa, which ended up being served by regulated entities but changed the payments landscape, I expect financial institutions to make inroads into the Metaverse. These include not only traditional financial institutions but also de novo digital banks and decentralized autonomous organizations (DAOs). This change will bring leverage, financing, loans and so forth, but it may have a unique metaverse flavor to it. This implies a protocol-driven model that provides exchange, value and collateral locking and borrowing — a glimpse of which we already see with concepts like DEX (decentralized exchanges), liquidity pools, automated market makers (AMMs) and NFT marketplaces.

Implication and challenges

The business of the Metaverse is complicated and not without pitfalls and uphill battles. Just like any new venture, it has a risk component, licensing or regulatory challenges, and staffing issues, and these challenges may be particularly acute for the Metaverse. The challenges include, but are not limited to, the following:

Regulation and compliance: The industry is aware of the changing attitudes and regulatory posture around the globe. There is a pervasive lack of regulatory clarity on basic digital assets, as there are many exotic tokens and digital assets emerging and entering the Metaverse. That is to say that taking advantage of what used to be regulatory arbitrage is now an impediment in the global movement of various asset classes in the Metaverse. The broader industry will need to dedicate some capacity to help craft a relevant and fair structure or framework.

Technology or protocol risk: Technological challenges around interoperability and identity are still massive roadblocks to the progress and promise of blockchain and, eventually, the Metaverse. If we want the Metaverse to go beyond modality and have an interchangeable mix of digital assets, we need it to be interoperable across various networks and universal ID transactions to be a seamless process with non-repudiation. Incidentally, this also will help with regulatory simplicity.

Talent: Industry has a profound shortage of talent, including technologists, token economists and business leaders, to create a team that can stay in place to build, maintain and improvise on projects. This is a huge issue. We also see so much capital chasing too few projects, which historically has never been a good balance to attract talent and incentivize the development, retention and commitment of the right people.

Related: Decentralization revolutionizes the creator’s economy, but what will it bring?

Conclusion

The Metaverse today is a representation of the rhetoric of interaction modalities. The promise to realize the vision relies on robust investment in Web3 infrastructure, regulatory and compliance frameworks and talent, which will enable the transfer of various value artifacts from one universe to another and adaptation of the value system of various networks with exchange, fungibility and interoperability. The seamless movement of user-controlled value in tokenized or data forms will render these modalities effective. We see glimpses of these today in the financialization of NFTs and decentralized finance (DeFi) constructs like DEXs, AMMs and DAOs.

So, I would say a revolution is underway. It is up to us to understand it, participate in it and monetize it.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision.

The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.