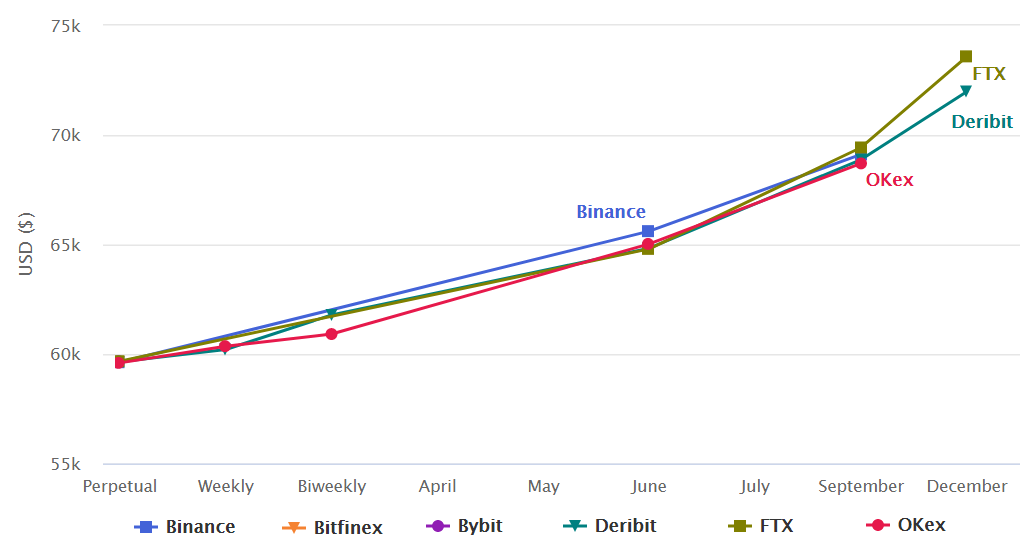

Bitcoin (BTC) has been struggling to break the $60,000 resistance for almost a month. But despite the impasse, BTC futures markets have never been so bullish. While regular spot exchanges are trading near $59,600, the BTC contracts maturing in June are trading above $65,000.

Futures contracts tend to trade at a premium, mainly on neutral-to-bullish markets, and this happens on every asset, including commodities, equities, indexes, and currencies. However, a 50% annualized premium (basis) for contracts expiring in three months is highly uncommon.

Unlike the perpetual contract — or inverse swap, these fixed-calendar futures do not have a funding rate. Thus, their price will vastly differ from regular spot exchanges. Fixed-calendar futures eliminates eventual funding rates’ spikes from the buyers’ perspective, which can reach up to 43% per month.

On the other hand, the seller benefits from a predictable premium, usually locking longer-term arbitrage strategies. By simultaneously buying the spot (regular) BTC and selling the futures contracts, one gains a zero-risk exposure with a predetermined gain. Thus, the futures contracts seller demands higher profits (premium) whenever markets lean bullish.

The three-month futures usually trade with a 10% to 20% versus regular spot exchanges to justify locking the funds instead of immediately cashing out.

The above chart shows that even during the 250% rally between March and June 2019, the futures’ basis held below 25%. It was only recently in February 2021 that such phenomena reemerged. Bitcoin surged by 135% in 60 days before the 3-month futures premium surpassed the 25% annualized level on Feb. 8, 2021.

While professional traders tend to prefer the fixed-month calendar futures, retail dominates perpetual contracts, avoiding the expiries’ hassle. Moreover, retail traders consider it expensive to pay 10% or larger nominal premiums, even though perpetual contracts (inverse swaps) are more costly when considering the funding rate.

While the recent 0.20% funding rate per 8-hour is extraordinary, it is definitely not unusual for BTC markets. Such a fee is equivalent to 19.7% per month but seldom lasts more than a couple of days.

A high funding rate causes arbitrage desks to intervene, buying fixed-calendar contracts and selling the perpetual futures. Thus, excessive retail long leverage usually drives the futures’ basis up, not the other way around.

As crypto-derivatives markets remain largely unregulated, inefficiencies shall continue to prevail. Thus, while a 50% basis premium seems out of the norm, one must remember that retail traders have no other means to leverage their positions. In turn, this causes temporary distortions, although not necessarily worrisome from a trading perspective.

While exorbitant funding rate fees remain, leverage longs will be forced to close their positions due to its growing cost. Thus, December’s $73,500 contract does not necessarily reflect investors’ expectations, and such a premium should recede.

The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.