An initial coin offering (ICO) for a blockchain project called Bancor has set a new industry record, raising $153m in ether, the native currency on the ethereum blockchain, as part of a crowdsale that concluded today.

Data shows a smart contract connected to the sale had collected more than 390,000 ether by the time it ended at 18:00 UTC, an amount worth $152.3m at current prices. As such, the figure is higher than even the funding raised by The DAO, the notorious failed fundraising project that made headlines last year when it lost the millions of investor funds it raised in a similar sale.

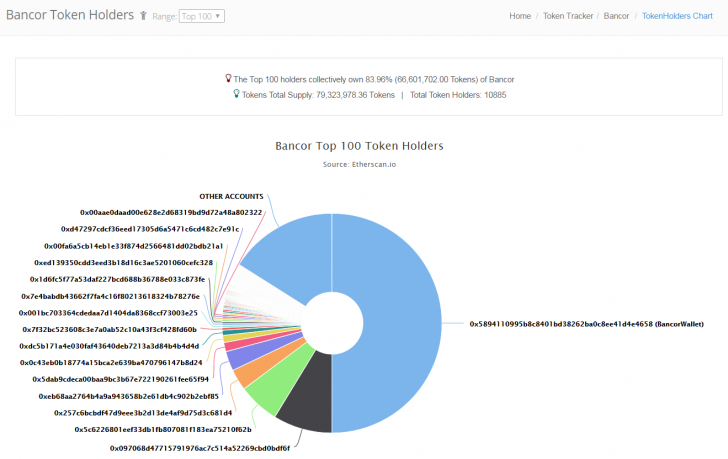

Overall, 79,323,978 Bancor network tokens (BNTs) were created as part of the ICO, with the top token holders now possessing 83.96% of the tokens, or 66,601,702 BNT. Fifty percent of the total tokens, or 39,661,989 BNT, were sold to the public, while the remaining 50% were allocated for future usage.

The ICO attracted 10,885 buyers, according to available data, with more than 15,000 transactions sent to the address for purchases during the sale.

Launched in 2017, Bancor, overseen by the Bprotocol Foundation, has been pitched as a platform designed to make it easier for users to launch their own blockchain tokens.

Of the remaining funds, a blog post by the company states the remaining funds will be directed toward partnerships, community grants, public bounties and project advisors.

Issues with the sale

As with past sales of this kind, the ICO was accompanied by reports of the ethereum network facing significant transaction loads, resulting in delays.

According to the Bancor website, the initial target was 250,000 ether. A transaction was set to limit the crowdsale to one hour after hitting 80% of this cap, but due to network disruption and delays, the crowdsale ended up lasting two additional hours.

Posts on social media suggest that at least some users saw transaction issues during the sale. One thread on Reddit drew complaints about their transaction being dropped 35 minutes after they sent it to the ICO address.

Some participants who spoke to CoinDesk also said that they had experienced delays in transacting, including one who had issues moving their ethers off an exchange for the purposes of participating in the ICO.

One exchange operator went so far as to argue that the ICO had increased transaction congestion, colorfully remarking that larger ether buyers were disrupting the sale.

Notable investors

Another factor contributing to the frenzy is that, as sale was getting underway, Bancor revealed that the project had attracted new and notable investors.

Among those announced to be contributing funds was investor Tim Draper of VC fund Draper Fisher Jurvetson. Though new to the ICO space – he previously backed the Tezos project ahead of its yet-to-be-held offering – Draper has invested in a number of bitcoin startups in the past few years.

In 2014, however, Draper made headlines when it emerged that he had bought 30,000 bitcoins during US government auction, later picking up an additional 2,000 BTC during a second sale. As part of the funding, Draper will also be joining the project as an advisor.

The Bancor sale was also backed by Blockchain Capital, an investment firm that focuses on startups in the space.

According to a blog post published today, Blockchain Capital is making its investment via its BCAP token, which it launched earlier this year.

‘Insane’ speculation

In the blockchain community, the reverberations of the sale were felt far and wide among market observers, many of whom expressed disbelief at the funding totals raised.

Some commentators, when reached by CoinDesk, simply responded by calling the investment ‘insane’. Likewise, when asked if the total raised was related to project’s fundamentals, Jaxx director of business and community and bitcoin entrepreneur Charlie Shrem simply responded: “No.”

Even proponents of the token sale model found fault with the sale.

Nic Tomaino, a former business development manager at Coinbase and principal at Runa Capital, remarked that he hadn’t been following the project due in part to the level of hype that it had attracted.

In particular, Tomaino took issue with how the project popularized news about investments in its token supply, noting the blog post that advertised investor Tim Draper’s personal contribution.

“Posting that the day of a token sale is not something that any team really building something valuable would do,” he told CoinDesk.

Still, others took it as a positive sign of market maturity. Among those to comment on the sale was JoyStream founder Bedeho Mender, who suggested that the raise had given him some pause, stating:

“As someone actually building a decentralized application on bitcoin, it really makes me think what I am giving up in terms of community support and funding by staying on the platform.”

Representatives for Bancor did not immediately respond to a request for comment.

ICO boom

The blow-out sale follows other offerings in recent weeks that have generated significant activity, putting new attention on the token sale model as a method of project capitalization.

More notable entries have included web browser startup Brave, which raised $35m at then-current ether prices in just under seconds. Gnosis, an ethereum-based prediction market, also attracted a bevy of speculators for its $12.5m sale in April.

Indeed, the ICO model has emerged as an alternative to traditional venture capital in recent months, though some observers have questioned whether the speculative frenzy taking place today is a healthy one.

Others still have criticized ICOs as vehicles for scams that take advantage of an uninformed public’s thirst for big gains in emerging technology.

Disclosure: CoinDesk is a subsidiary of Digital Currency Group, which has an ownership stake in Brave.

Calculator image via Shutterstock

steals Dogecoin’s thunder")